Why Smart People Make Terrible Money Decisions

Intelligence doesn't protect you from bad financial choices. Discover the 5 psychological traps — backed by real research — that trip up even the smartest people with money.

You're Smart. So Why Is Your Bank Account Disagreeing?

You know you should save more. You've read about compound interest. You understand diversification. You've even told others not to panic-sell during a market crash.

And yet.

You bought that thing you didn't need. You held onto that bad investment too long. You spent money you meant to save — again.

Here's the uncomfortable truth most personal finance content refuses to say: your intelligence isn't the problem, and it isn't the solution either.

In fact, research shows that higher intelligence can make certain money mistakes worse.

This is Think Smarter — a series about the science of how we actually think, decide, and behave. Not how we think we do. How we actually do.

The Myth: Smart = Good With Money

Traditional economics was built on a comfortable lie: that humans are rational beings who make logical decisions based on available information.

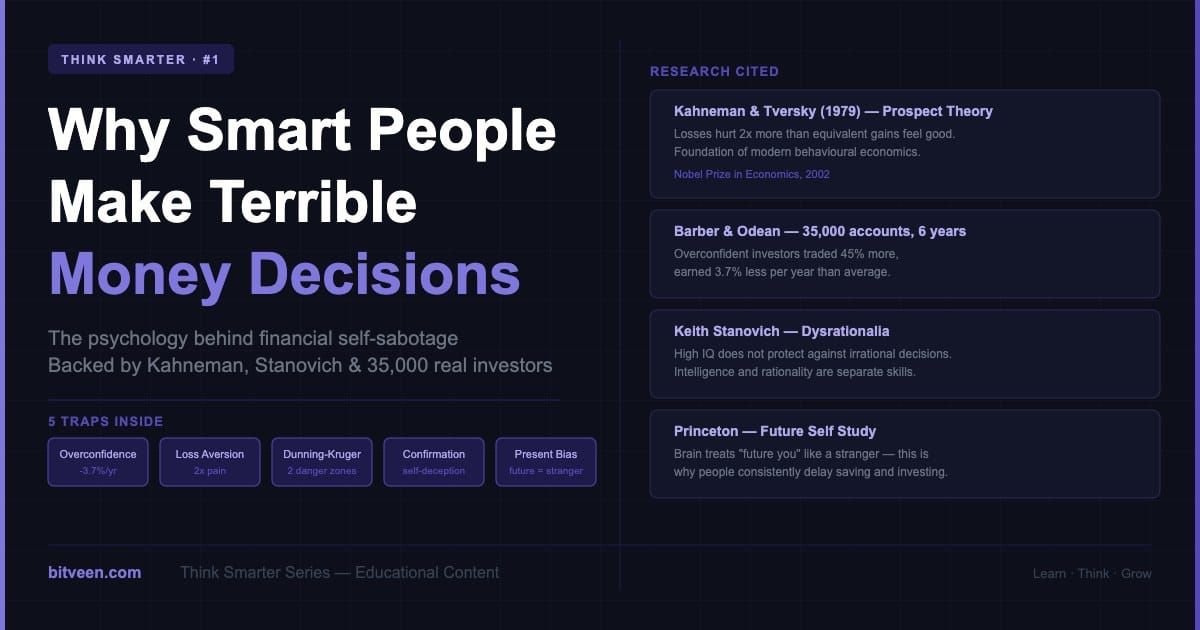

Psychologist Keith Stanovich at the University of Toronto spent over a decade studying this. His conclusion? IQ tests measure logic, abstract reasoning, and processing speed well. But they don't measure rationality — the ability to make decisions that actually serve your long-term interests.

He calls this gap "dysrationalia": the inability to think and behave rationally despite having adequate intelligence.

Translation: you can be genuinely smart and genuinely terrible at decisions. These are entirely separate skills.

Warren Buffett has said it directly: "Investing is not a game where the guy with the 160 IQ beats the guy with the 130 IQ." His edge isn't intelligence — it's behaviour.

5 Psychological Traps That Catch Smart People Off Guard

1. Overconfidence — The Smarter You Are, The Bigger This Gets

The more you know about a subject, the more confident you become. And the more confident you are, the less you question yourself.

Researchers Barber and Odean studied 35,000 investor accounts over six years. Their finding: overconfident investors traded 45% more than average, and earned 3.7% less per year as a result. More activity, worse outcomes.

The classic example: a software engineer who understands tech deeply invests their entire portfolio in tech stocks. "I understand this industry." But understanding an industry is not the same as predicting its stock price. The 2000 dot-com crash wiped out thousands of people who genuinely understood the internet.

Intelligence amplifies overconfidence. Smarter people construct more elaborate, convincing justifications for their decisions. They can always find a reason their choice was right. This is called motivated reasoning — and a higher IQ just means a better internal lawyer.

2. Loss Aversion — Feeling Losses Twice as Hard as Gains

In 1979, psychologists Daniel Kahneman and Amos Tversky published one of the most cited papers in psychology history. Their finding: humans feel the pain of losing £1,000 roughly twice as intensely as the pleasure of gaining £1,000.

This sounds like a small quirk. It isn't.

It means people hold losing investments far too long — "I'll sell when it gets back to what I paid." It means people avoid investing during downturns — when historically that's exactly the best time to buy.

Smart people construct better narratives around their loss aversion:

- "I'm not panic-selling. I'm being prudent."

- "I'm not holding a loser. I'm being patient."

The loss aversion is identical. The justification is just more sophisticated.

The Loss Aversion Test

Two scenarios. Same maths. Watch how your gut reacts differently.

SCENARIO A

You just gained ₹10,000 in your portfolio this week.

How does that feel?

SCENARIO B

You just lost ₹10,000 in your portfolio this week.

How does that feel?

3. The Dunning-Kruger Curve — Two Danger Zones, Not One

Everyone knows the first part: beginners overestimate how much they know. But there's a second, less-discussed danger zone — the one that catches smart, high-achieving people specifically.

As people become genuinely expert in one field, they often assume that expertise transfers. A doctor assumes they're a good investor. An engineer assumes they can read financial markets. A lawyer assumes they can negotiate business deals.

Danger Zone 2 is where high-achievers live. It's rarely talked about — because the people inside it are too confident to notice.

4. Confirmation Bias — Your Brain Only Googles One Side

Once you've made a financial decision, your brain quietly filters information. Evidence supporting your choice gets absorbed. Evidence contradicting it gets dismissed as "biased" or "missing context."

Psychologist Jonathan Haidt describes the brain as a lawyer who has already decided the verdict: it only looks for evidence that supports the case.

The more articulate you are, the better you are at lying to yourself. A finance PhD can construct a 10-point argument for keeping a bad investment. A less-informed person might just shrug and admit "I don't know" — which is often the more honest answer.

5. Present Bias — Future You Is a Stranger

Ask anyone: "Would you prefer £100 today or £110 next week?" Most people take the £100 now.

Ask differently: "Would you prefer £100 in 52 weeks or £110 in 53 weeks?" Most people wait for the £110.

Economically, these are identical choices — one week's wait for 10% more. But psychologically they feel completely different. This is present bias: the tendency to overvalue immediate rewards and discount future ones. It's why we tell ourselves we'll start saving "next month." Next month always becomes next month.

Research at Princeton showed something startling: when people think about their future selves, the brain activates the same regions as when thinking about a complete stranger. Your future self is neurologically someone you don't know well. So naturally, you don't make sacrifices for them.

Smart people know this research. And they still do it. Because knowing a bias exists doesn't deactivate it.

Which Money Bias Traps You Most?

Answer 3 quick scenarios. Get your dominant bias revealed instantly.

So What Actually Helps?

You can't think your way out of these traps. They're not logic errors — they're psychological architecture. But you can build systems that work around them.

- For overconfidence: Set rules before you invest, in a calm state. "I will not put more than 10% in any single stock." Rules made when calm protect you from decisions made when excited.

- For loss aversion: Automate your investments. SIPs (Systematic Investment Plans) remove the active decision — so loss aversion has nothing to grab onto.

- For confirmation bias: Actively seek the strongest argument against your position. Not to destroy it — to stress-test it. If you can't articulate why you might be wrong, you don't understand your position as well as you think.

- For present bias: Make your future self concrete. Give them an age and a situation. "57-year-old me needs this money." Specificity makes the future self less of a stranger.

- For all biases: Write down your reasoning before making any major financial decision. Then come back and read it 48 hours later. Distance reveals what emotion hides.

The One-Sentence Takeaway

Financial intelligence isn't about IQ. It's about knowing your brain will lie to you — and building systems that tell the truth anyway.

What's Next in Think Smarter

The next blog tackles something even more counterintuitive: why earning more money often makes people feel poorer — and the psychological phenomenon called hedonic adaptation that explains why your last pay rise didn't make you as happy as you expected.

→ Subscribe to Bitveen to get it first

DISCLAIMER

This article is for educational and informational purposes only. The psychological research and examples discussed are intended to help readers understand behavioural patterns — they do not constitute financial, investment, or professional advice. Every individual's financial situation is different. Please consult a qualified financial advisor before making any investment or financial decisions. Bitveen.com is not responsible for any financial decisions made based on the content of this article.